More than two in five Americans now live with obesity, and 279,000 people chose bariatric surgery in 2022 (cwcc.org). If you’re comparing Colorado clinics, one question towers above the rest: why does the “$12,000 gastric sleeve” you see online rarely match the bill you pay?

We’re parents, partners, and busy professionals juggling mortgages, soccer runs, and college funds. Beyond the surgeon’s fee, you’ll need to plan for childcare, time off work, and even protein shakes.

This guide keeps you ahead—comparing real self-pay prices, flagging hidden fees, and outlining funding tactics. You’ll also get a quick-fire checklist and a direct link to pre-surgery planning so you can budget with eyes wide open.

Colorado price snapshot: what clinics quote

Search “gastric sleeve Denver” and price tags scatter. One center lists a $11,337 self-pay bundle, another markets an $11,800 “all-inclusive” sleeve, while a large hospital promotes a $4,500 surgeon fee then separates every other charge. A recent side-by-side review published on HackMD of five Front Range providers shows clear clusters: self-pay sleeves sit between $11,000 and $13,000; gastric bypass packages climb to $16,000–$20,000; and any “surgeon fee only” offer balloons once anesthesia and facility costs appear.

Why the spread? Setting drives price. Public hospitals negotiate lower cash rates but add charges for consults and labs. Private bariatric centers bundle those preliminaries and may include extras such as nutrition coaching or robotic techniques. Operating inside a large hospital system can add thousands because room overhead is higher than in a stand-alone surgical center.

The clinic also publishes a full line-item cost sheet that flags its separate $450 surgical-assistant fee—exactly the sort of detail you want clarified before signing consent forms.

Even with those variables, Colorado stays on the lower end of U.S. cash pricing. National averages run $14,000 to $23,000 for a sleeve, so families here already start a few thousand dollars ahead. That edge matters only if you know what each quote covers—a puzzle we address in the next section.

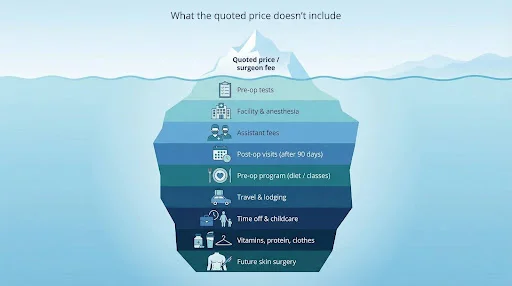

What the quoted price leaves out

1. Pre-op evaluations and tests

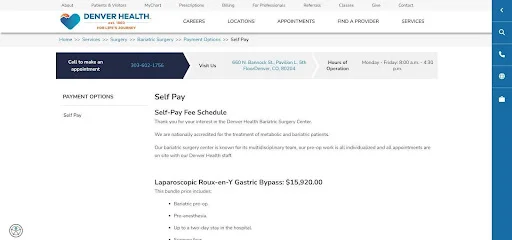

The advertised price usually covers only the surgeon’s part of a longer process. Before you reach the operating room you must clear several checkpoints: surgeon consult, nutrition visits, psychological screening, blood work, an EKG, and sometimes a sleep study. Denver Health lists its sleeve at $11,337, yet itemizes more than $1,500 in extra pre-op charges—$155 for the first consult, $56 per dietitian visit, $200 for the mental-health evaluation, and $205 in labs (Denver Health Self-Pay Bariatric Fee Schedule). All are mandatory.

Denver Health bariatric self-pay fee schedule screenshot

Ask for an itemized estimate that covers every appointment. If a clinic bundles pre-op work, great. If not, add those figures early so surprises do not derail your plan.

2. Hospital facility and anesthesia fees

Surgeon talent is only part of the bill. The operating room, circulating nurses, and the anesthesiologist each have their own prices. Some private clinics combine these costs; large hospital systems often separate them.

A Denver center advertises a $4,500 surgeon fee. Families celebrate, then watch the facility charge, anesthesia invoice, and sterile-processing line appear, lifting the final total into the familiar $15,000–$20,000 range (Denver Health Self-Pay Bariatric Fee Schedule).

Confirm in writing that your quote includes the operating suite, anesthesia, and an overnight stay if needed. If any part feels vague, assume it is not included.

3. Surgical assistant fees

Bariatric surgeons rarely work alone. A certified first assistant or second surgeon helps manage instruments and watch for complications. Their fee often sits outside the headline price.

One metro clinic lists an $11,800 “all-inclusive” sleeve, then footnotes a $450 assistant fee. Denver Health’s schedule handles the charge the same way. Ask whether an assistant is required and who pays the bill. A quick question today saves a surprise invoice later.

4. Post-op follow-ups beyond the global window

Most self-pay bundles promise “all follow-ups included,” but coverage ends after the global period, usually 90 days. Day 91 turns the meter back on.

Denver Health spells it out: six-month and one-year visits cost $99 each, and routine nutrition labs at three, six, and twelve months add $400 to $500 in the first year. Private clinics may extend care to a full year, but only if that perk appears in writing. Ask exactly how many visits, labs, and dietitian check-ins the fee covers, then budget for the rest.

5. Pre-op program requirements

Some surgeons and almost every insurance plan require a supervised diet or lifestyle program before surgery. A six-month nutrition class can run a few hundred dollars and almost never hides inside the surgery quote.

One Denver program charges about $400 for its pre-op nutrition series. Cash-pay patients may skip insurance paperwork yet still face surgeon-mandated milestones such as losing five percent of starting weight. Ask whether a formal program is required, how many visits it involves, and who pays.

6. Travel and lodging

Colorado is a large state. If you live in Durango, Grand Junction, or a mountain town, every appointment means fuel, tolls, and sometimes lodging. Even Front Range families may choose an out-of-state or Mexico clinic, trading lower surgical fees for airfare and hotels.

Two round-trips for consults, one longer stay for surgery, and a companion’s flight can easily total $1,000. Some clinics negotiate hotel discounts; ask for any codes and try to combine appointments in one trip.

7. Time off work and childcare

Surgery lasts a few hours; recovery lasts weeks. Most sleeve patients need two to four weeks away from strenuous work. If paid leave is limited, factor lost wages into the real cost. A three-week gap at a $1,000-per-week paycheck equals $3,000.

Home life continues. Someone must drive children, lift groceries, and handle chores while you ease back into solids. Even a $20-per-hour sitter for four hours a day over two weeks adds $1,120. Plan coverage early so recovery feels calm, not chaotic.

8. Long-term health maintenance

Weight-loss surgery is a one-day procedure with lifelong maintenance. Daily bariatric vitamins, calcium, and B-12 cost $20 to $50 a month. Early on, protein powder can add $60.

Shrinking sizes mean new clothes. Many patients cycle through three wardrobes in year one. Thrift stores and resale apps help, but set aside a clothing fund so success feels rewarding, not stressful.

The upside: many patients reduce or drop blood pressure or diabetes medications within months. Track both outgoing and incoming costs to see the full picture.

9. Body contouring surgery

Rapid weight loss can leave extra skin. About seven in ten bariatric patients consider a tummy tuck, arm lift, or body lift once their weight stabilizes. Insurers usually label these elective, so the bill is yours.

A basic abdominoplasty starts around $5,000; an extended lower-body lift can top $15,000. Add anesthesia, facility fees, and time off work, and the total rises. Some clinics help document medical issues so insurance pays a portion, but approval is never certain.

View skin surgery as a future option. If it stays on your wish list, start a small savings line now so you are ready when your surgeon gives the all-clear.

Self-pay vs. insurance: which route saves you more?

Insurance coverage in Colorado

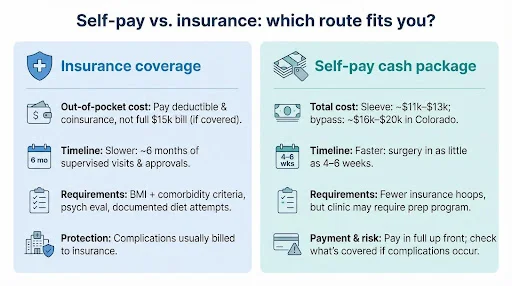

If your health plan covers bariatric surgery, you hold a golden ticket that can shrink a potential $15,000 bill down to your deductible, coinsurance share, and maybe a modest hospital copay. Most major carriers in Colorado—Anthem, Cigna, Kaiser, and United—approve sleeves or bypasses once you clear their checklist: a body-mass index of forty (or thirty-five with a serious condition), a psychological evaluation, and roughly six months of supervised weight-loss visits.

These hoops serve two purposes. They prove medical necessity to the insurer and give you time to practice the habits surgery will lock in for life. The trade-off is waiting. Gathering doctor notes, diet logs, and prior authorization can stretch the timeline to six months or more. Yet for families who have already met their deductible—or those who plan surgery early in a new benefits year—the savings often outweigh the delay.

Employer plans sometimes exclude bariatrics, and smaller group policies may cap benefits. If that happens, pivot to an ACA exchange plan during open enrollment. Colorado marketplace policies are required to cover weight-loss surgery, so a strategic one-year switch may raise monthly premiums but still costs far less than paying the full fee yourself.

In short, if coverage exists, use it. Even a high-deductible plan that leaves you with $4,000 to $5,000 out of pocket usually beats writing a check for the entire procedure.

Self-pay cash packages

When insurance excludes bariatrics—or when you prefer not to wait—cash packages step in. Colorado clinics offer flat-fee bundles that include the surgeon, anesthesia, operating room, and short-term follow-up. A gastric sleeve runs $11,000 to $13,000; a bypass lands around $16,000 to $20,000. Compared with national averages, those figures feel manageable.

Speed is the biggest perk. Skip the six-month diet requirement and you can move from consult to operating room in as little as four to six weeks. No phone tag with insurers, no prior-auth denials, and no appeal letters.

The challenge is payment. Clinics normally expect the full amount before surgery, so many families line up financing. (We cover loan options in the next section.) One immediate tip: negotiate. Providers often shave a few hundred dollars off for debit payments or bank transfers because they avoid credit-card fees.

Finally, protect yourself on complications. Some cash bundles include a thirty-day safety net that discounts any return to the operating room; others leave you fully responsible. Read the clause, then keep an emergency fund or maintain a high-deductible insurance plan for unexpected events. That small precaution buys peace of mind.

Financing options: turning a big bill into manageable payments

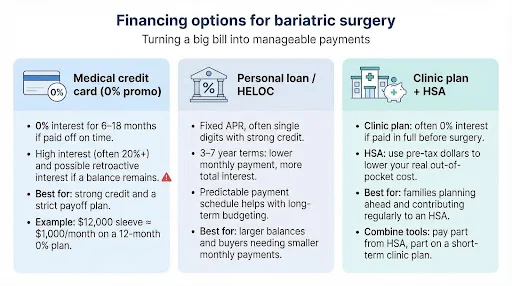

Medical credit cards (CareCredit and others)

Medical credit programs such as CareCredit, Alphaeon, or Synchrony’s Health & Wellness card offer short promotional windows—six, twelve, or eighteen months—with 0 percent interest. Divide your surgery cost by the number of months and commit to that payment. A $12,000 sleeve on a twelve-month plan equals $1,000 per month.

Late payments or a remaining balance after the promo period trigger retroactive interest, often 26 percent. Set automatic payments and treat the payoff date as fixed. Longer terms of forty-eight or sixty months start with interest from day one, typically 14 to 17 percent APR for strong credit and higher for weaker scores.

Before signing, confirm the exact promotional length, ask whether a down payment lowers the principal, and verify that billing begins after surgery, not at application.

Personal loans and lines of credit

If the zero-interest window feels too tight, a personal loan spreads the cost over three to five years at a fixed rate. Credit unions often post single-digit APRs; online lenders average 9 to 15 percent. Home-equity lines can fall lower because your house backs the note.

For example, a $15,000 loan at 8 percent over four years costs $366 per month and about $3,100 in interest. Stretching to seven years drops the payment to $228 but more than doubles interest. Shop for pre-qualification quotes, compare terms, and choose the shortest schedule you can handle without strain.

Confirm that funds deposit to your account so you can negotiate a discount for paying the clinic up front, and look for a lender with no prepayment penalty.

In-house payment plans and HSA funds

Some clinics act as their own bank. They take a down payment—often 50 percent—then spread the balance over six or twelve months interest-free, provided every dollar clears before surgery. This works for families expecting a tax refund or bonus within a few months.

Health Savings Accounts add another layer. Dollars already in an HSA skip federal tax on the way in and the way out, as long as you spend them on qualified medical care. Weight-loss surgery qualifies. Max out contributions the year before surgery, use the HSA card for part of the bill, and you immediately save about 22 to 30 percent depending on your bracket.

Pairing these tools is powerful: pay half from pre-tax HSA funds, finance the rest interest-free with the clinic, and start recovery owing only predictable monthly transfers you already planned.

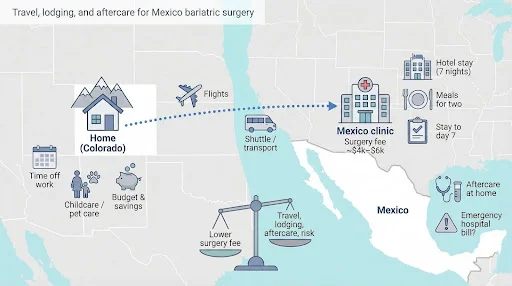

The Mexico temptation: big savings, bigger homework

Why prices plunge south of the border

Tijuana billboards tout gastric sleeves for $4,000 to $6,000, less than half the typical Colorado bundle. Lower hospital overhead, slimmer staff salaries, and exchange-rate advantages create that gap. Add concierge service and no insurance hurdles, and thousands of Americans cross the border each year.

Lower price does not mean lower standards. Top Mexican centers feature U.S-trained surgeons, Joint Commission International accreditation, and complication rates similar to stateside hospitals. Risks rise only when patients chase the rock-bottom quote without vetting credentials.

Confirm the surgeon’s board certification, hospital accreditation, and annual bariatric volume. Look for hundreds of independent reviews, not just curated testimonials. Request leak-rate and infection data in writing, and be sure the package covers at least two nights in a monitored hospital room rather than a hotel recovery suite. When those boxes are checked, savings can remain strong even after flights, a companion ticket, and lodging.

Travel costs, aftercare, and risk math

Airfare and hotels narrow the gap faster than most people expect. Two round-trip tickets from Denver to San Diego, a shuttle to Tijuana, seven hotel nights, meals for two, plus pet or childcare at home often total $1,000 to $1,500. Add that to a $5,500 Mexico sleeve and the bill lands near $7,000—still below Colorado rates but no longer stunning.

Serious complications, while uncommon, usually surface within the first week. Plan to stay near the clinic until day seven. Once home, you will need a local physician willing to order labs and inspect incisions. Some bariatric teams charge extra to adopt international patients; others decline.

Quick self-audit:

- Can you cover an emergency U.S. hospital bill if a leak occurs after you land?

- Do you have paid leave or flexible work to add travel days on top of recovery?

- Will a stateside bariatric team sign on for follow-up labs and nutrition visits?

If you can answer yes and trust your vetted surgeon, Mexico may deliver solid savings. If not, any complication or logistical snag can erase the discount. Do the math, review your safety net, and place peace of mind at the center of your decision.

Weighing the costs and the payoff

Money leaves your bank account the day you schedule surgery; health dividends roll in for decades. Studies show that adults living with obesity spend 81 percent more on medical care than peers at a healthy weight, mainly on prescriptions, doctor visits, and hospital stays. When surgery resolves diabetes, high blood pressure, or sleep apnea, those monthly co-pays and device rentals often disappear.

Patients feel the benefit long before insurance data reflect it. Energy climbs, joints ache less, and family hikes last longer. On RealSelf, 98 percent of gastric sleeve reviewers mark the procedure “Worth It,” a score that beats many cosmetic treatments. That figure represents people who traded one expense line for another and gained extra life moments in return.

Treat the decision like an investment: up-front capital versus long-term return. Add every hidden fee we covered, then estimate what you will save once insulin, CPAP supplies, or hypertension prescriptions no longer hit the budget. Many Colorado families break even within two to three years. After that, gains keep growing—more playtime with children, fewer sick days, and vacations enjoyed on foot instead of from a bench.

Conclusion: plan every dollar, invest in every tomorrow

Weight-loss surgery is not a one-tap payment. It is a sequence of smart financial choices that open the runway to lifelong health. We have covered headline prices, hidden fees, funding strategies, and even the appeal of an international option. The next move belongs to you.

Print an itemized quote, download our checklist, and open your family calendar. Plot the pre-op tasks, the recovery help, and the payment path that fits your real life. If you need a starting point, visit our pre-surgery planning guide, then circle a date that turns intention into action.

Every dollar you allocate today buys energy, longevity, and moments with the people who matter most. That return outshines any hidden fee. Move forward with eyes open and budget balanced, and Colorado’s bariatric journey can pay dividends for decades.